In New Zealand Traded Endowment Policies (TEPs) are little known and have lived on the fringes of investment options. But to those who know them, TEPs have been solid, proven performers offering a unique low-risk investment alternative.

As the investment climate changes (low interest rates ,housing policy changes) this investment option comes into sharper focus. Investors are looking outside the box for alternatives and TEPS, being lower-risk, tax-free investments, are gathering interest.

Below we want to explore this lesser-known investment opportunity. To do that we speak directly to the offerings of Policy Exchange, as New Zealand’s only provider. Policy Exchange began in 1995 and currently administers close to $20.0m on behalf of private individuals and trusts.

What are Traded Endowment Policies?

Traded Endowment Policies or “TEPs” are investment-backed endowment and whole of life insurance policies that have been acquired from the original policyholder by Policy Exchange, then made available for investment.

At all times, whether owned by the original policyholder or a subsequent investor, the policy remains an issuance of the original life company. This is an important point when considering the relative strength of a Traded Endowment Policy investment.

Key Characteristics

TEPs are generally described as a fixed interest alternative, with similar attributes, albeit with a slight twist.

Below is a summary of common features shared by all TEPs.

Security– ‘Locked In’ Maturity Value

Each policy includes an amount payable at maturity that is a fixed contractual obligation of the issuing life company.

Referred to as the ‘Locked In’ Maturity Value, this offers a strong layer of protection for investors.

Strong Financial Strength Ratings

The Reserve Bank requires all life companies in New Zealand to obtain an independent “Insurer Financial Strength Rating” from international ratings agencies such as Standard & Poors.

This provides investors a benchmark for assessing the ability of the issuing life company to meets its obligations to policyholders as they fall due.

AMP Life, for example, currently hold an A- “Strong” rating from Standard & Poors.

Tax-Free Returns

The amount paid out by the life company at maturity is considered to be a capital receipt and therefore free of tax.

Conservative Growth Rate Assumptions

All quoted returns are projections, with the amount paid at maturity dependent on the level of future bonuses (or earnings) declared and added to the ‘Locked In’ Maturity Value by the issuing life company each year.

However, all policies offered via Policy Exchange are priced against the more conservative ‘Low’ Projections Rates used by the life company. These rates are typically 20% less than the declared earnings rates prevailing at the point of investment, and provide a layer of protection should future bonus rates fall below the prevailing declared rates.

Fixed Durations

Each policy has its own fixed maturity date: Durations typically range from 4 to 10years.

Select Stock to fit Your Requirements

Each Traded Endowment Policy has its own unique blend of the above key characteristics. These are clearly represented on a weekly stock list, and investors can select the item that best suits their needs. Some investors prefer greater levels of security with lower offered returns, whilst others are happy to take slightly lower levels of security with higher offered returns. All TEPs, however, enjoy the buffer offered by Policy Exchange pricing against the ‘Low’ Projection Bonus (or earnings) Rates.

Who is this product for?

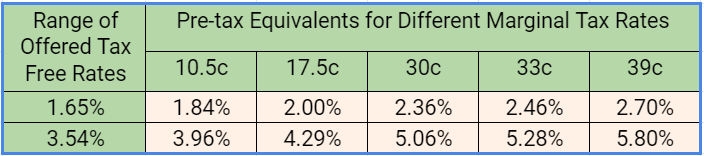

Lower-risk is the keyword that attaches this product to investors who are 5 – 10 years away from retiring, or those in retirement who are risk averse. This is the obvious lifecycle-match but any portfolio benefits from a mix of risk levels. The advantage of buying TEPs is that they reach maturity at a set date, which is useful, for example, if you need to pay school fees in a certain year. As the following table demonstrates, the tax-free element benefits those on a higher tax rate.

A powerful part of this product is the ability to choose your own policy from a weekly stock list. This will determine your maturity date and projected returns, allowing you to further tweak your level of risk.

Here’s 3 examples taken off Policy Exchange’s Sample Stock list:

Policy Exchange item number: 4293

Purchase price: $225,023.20

Annual premium due: Nil

'Locked In' Maturity Value - $: $187,452.00

'Locked In' Maturity Value - %: 83.30%

Projected ‘Low’ Maturity Value - $248,232.54

Projected Tax-Free Return based on the ‘low’ maturity value projection: 2.53%

Projected Pre-Tax Equivalent Return at highest tax rate: 4.15%

Policy Exchange item number: 4287

Purchase price: $53,141.17

Annual premium due: Nil

'Locked In' Maturity Value - $: $50,639.00

'Locked In' Maturity Value - %: 95%

Projected ‘Low’ Maturity Value - $58,700.36

Projected Tax-Free Return based on the ‘low’ maturity value projection: 1.99%

Projected Pre-Tax Equivalent Return at highest tax rate: 3.26%

Policy Exchange item number: 4284

Purchase price: $84,477.66

Annual premium due: $3,220 x 7yrs

'Locked In' Maturity Value - $: $107,655.50

'Locked In' Maturity Value - %: 100%

‘Low’ Maturity Value - $119,758.00

Projected Tax-Free Return based on the ‘low’ maturity value projection: 1.62%

Projected Pre-Tax Equivalent Return at highest tax rate: 2.82%

TEPs can be exited at any time by either surrender to the life company or sale back to Policy Exchange. However, the exit price is generally at a discount to its underlying worth. Investors should expect to remain for the full investment term in order to achieve the best return outcome.

For more info: www.policyexchange.co.nz

See our Markets page for latest investment listings.